|

| Home>Investment & Treasury Center>Range of Products>Premium Accounts |

|

|

|

| Premium Accounts - Personalized banking solution with a touch of innovation. |

|

| If you are looking to counter the low interest rates through an innovative investment solution, Premium Account could be for you. Premium Accounts are short-term, currency related Investment accounts that provide you with an exciting opportunity to potentially earn a higher interest rate as compared to a conventional Time Deposit. |

|

The higher interest rate is because you accept the possibility that, at maturity of the Premium Account, you may be paid your Principal + Interest in another currency based on the choices taken while booking. The product is offered in the following currencies (USD, EUR, GBP, JPY, CHF, AUD, NZD & CAD). |

|

|

|

|

|

| Premium Accounts provide multiple benefits: |

|

- You benefit from the significantly higher interest rates on your principal

- Product is tailor-made to suit your individual view and needs

- If you are holding a currency that is expected to depreciate, then you benefit from the higher interest rates

- You may have professional/ personal need for two or more currencies and hence are indifferent to holding any of the two currencies. Premium Accounts offer you opportunity to be part of the FX markets and earn higher interest rates because you may be paid back in another currency as chosen at booking.

- You can maintain your liquidity with Premium Accounts through the tenor flexibility that we offer. Tenors range from 7 days to 180 days.

|

|

| Is Citibank Premium Account for you? |

|

| When investing in a Citibank Premium Account timing, choice of currencies and your personal investment preferences are all crucial. You might find a Citibank Premium Account particularly suited to you: |

|

- If you are indifferent to the two currencies chosen.

In other words, you are comfortable receiving your money in either the base or the alternate currency.

- If you wish to hold on to a particular currency that is weakening.

By investing in this currency in a Citibank Premium Account, you may earn a potentially higher interest, plus you may also have a chance of receiving your money back in the same currency.

- If you have the view that the exchange rate between the two currencies you have chosen appears to be stable.

In this case, the limited exchange rate movement between the currencies will help to improve your interest differential gains.

|

| Follow these steps: |

|

| 1. Select your Investment Parameters: |

|

| Your investment strategy is reflected in your selection of the following Investment Parameters. |

|

|

|

| A. |

Currency Pair comprises of the currency in which you will make available your investment amount (Base Currency) and a second currency which you are prepared to receive on maturity (Alternate Currency). |

|

|

Below is the range of currencies available for investing. You can select your Base Currency and Alternate Currency from the range. |

|

|

|

|

|

| B. |

Investment amount can start from as low as USD 25,000 or equivalent. |

|

|

| C. |

Investment tenor is the period of your investment. You can select your tenor from 1 week to 3 months as shown below. |

|

|

|

|

|

Please note that upon establishing your Premium Account successfully, the investment tenor is locked and cannot be altered till maturity. |

|

|

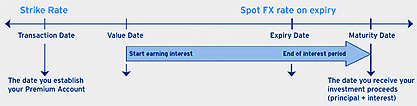

Each Premium Account tenor has 4 important dates to note. |

|

|

Transaction Date: The date you establish your Premium Account successfully. |

|

|

Value Date: The date on which Citibank accepts the investment amount from you (usually by debiting your Citibank account) and the date from which you will start earning interest. This date is normally the same as the Transaction Date. |

|

|

Expiry Date: The date Citibank determines whether to pay the proceeds of your investment in the Base Currency or the Alternate Currency. This is normally two business days before the Maturity Date. |

|

|

Maturity Date: The date on which the proceeds of your investment is repaid. |

|

|

|

|

|

| D. |

Differential from Spot and Strike Rate |

|

|

The Differential from Spot and Strike Rate determine the interest yield of your Premium Account. |

|

|

Differential from Spot: The difference between Spot Rate of your Currency Pair at the time of investment and Strike Rate. |

|

|

Spot Rate: The prevailing exchange rate for your selected Currency Pair. |

|

|

Strike Rate: The predetermined exchange rate you choose. Your proceeds will be converted into your Alternate Currency at this rate on Expiry Date. |

|

|

The greater the difference between Spot Rate on Transaction Date and the Strike Rate (in other words, the higher the Differential from Spot), the less likely you will receive your Alternate Currency upon maturity. |

|

|

| 2. How to choose the Differential from Spot & Strike Rate? |

|

| A. |

Interest yield has an inverse relation with the Differential from Spot. A lower Differential from Spot has a potentially higher potential interest yield. |

|

|

|

Strike Rate

(determined by you) |

|

Differential from Spot

(determined by you) |

|

Interest Yield

(computed by system) |

|

|

Nearer to Prevailing

Spot Rate |

|

Lower Differential

from Spot |

|

Higher Interest Yield |

|

|

|

Further from Prevailing Spot Rate |

|

Higher Differential

from Spot |

|

Lower Interest Yield |

|

|

|

|

|

|

| B. |

If you want to receive the returns of your investment in the same currency that you invested in (Base Currency), you may want to choose a higher Differential from Spot so there is a lower probability of getting converted into the Alternate Currency. |

|

|

However, if you want to receive the investment in the Alternate Currency or are indifferent in receiving either currency, your strategy may be to place a smaller buffer (smaller Differential from Spot), thereby allowing you to earn a higher interest yield. |

|

|

|

Differential from Spot (you choose) |

|

Probability of receiving your investment proceeds (principal+ interest) in the Base Currency (upon maturity) |

|

Probability of receiving your investment proceeds (principal+ interest) in the Alternate Currency (upon maturity) |

|

|

Higher |

|

Higher |

|

Lower |

|

|

|

Lower |

|

Lower |

|

Higher |

|

|

|

|

|

|

| C. |

Do you prefer to hold the Base Currency or Alternate Currency upon maturity? |

|

|

|

Preference Upon Maturity |

|

Differential from Spot |

|

Strike

Price |

|

Tenor |

|

Interest Yield % |

|

Investment Strategy |

|

|

Base Currency |

|

Higher |

|

Further from Prevailing Spot Rate |

|

Shorter Tenor |

|

Lower Interest Yield |

|

Conservative |

|

|

|

Alternate Currency |

|

Lower |

|

Nearer to Prevailing Spot Rate |

|

Longer Tenor |

|

Higher Interest Yield |

|

Aggressive |

|

|

|

|

|

|

To summarize overall, the selection of your Differential from Spot is dependent on your investment objective. |

|

|

| 3. Currency determination and maturity |

|

| On the Expiry Date, which is usually one/two business days before the Maturity Date, Citibank at its sole and absolute discretion will determine whether the proceeds (principal + interest) of your investment will be repaid in the Base Currency or the Alternate Currency. This will depend on a comparison between the Strike Rate which you have selected and the prevailing Spot Rate for your Currency Pair on the Expiry Date. Your proceeds will be returned to you in the Base Currency if the Spot Rate on Expiry Date did not reach or exceed the Strike Rate previously determined by you at the start of the Premium Account. |

|

| Here is an example** |

|

| Assuming that you have invested USD 100,000 in a one-week Citibank Premium Account, with USD as your base currency and British Pounds (GBP) as your alternate currency. |

|

|

Select base currency |

|

USD 100,000 |

|

|

Select alternate currency |

|

GBP |

|

Select tenor |

|

1 week |

|

|

Select preferred GBP/USD

strike price |

|

1.5500 (Assuming the current market for

GBP/USD is 1.5550 and you do not mind

diversifying into GBP at a preferred price of 1.5500) |

|

Interest rate |

|

7.57% p.a.* |

|

|

Interest Earned |

|

USD 147.19 |

|

|

|

| On Maturity: |

|

|

|

|

Scenario 1 |

|

Scenario 2 |

|

|

Rate on Expiry Date1 |

|

USD Weakens to 1.5650 |

|

USD Strengthens to 1.5400 |

|

Payout Currency^ |

|

Principal and interest

will be paid in USD |

|

Principal and interest

will be paid in GBP |

|

|

Principal + Interest received |

|

USD 100,147 |

|

GBP 64,610

(USD 100,147/1.5500) |

|

|

|

| * This is an indicative rate for a USD Premium Account of USD 100,000 with GBP as the alternate currency, strike price 50 points away from the prevailing spot rate as of April 29, 2013 for a one-week tenor. |

|

| ** The above is for demonstration purposes only and shall not be construed as investment advice. Citibank does not offer investment or tax advice to its customers. |

|

1Expiry Date is 2 business days before maturity date.

^ In the event that the market rate on Expiry Date is equal to the strike price, the Bank reserves the right to pay your principal plus interest in either the base currency (USD 100,147) or the alternate currency (GBP 64,610). |

|

|

| To apply for a Premium Account, please visit your nearest branch where our relationship manager will assist you in the account opening process including assessment of your investor profile and your knowledge and experience. |

|

| If you would like a Citibank relationship manager to call you, please click here |

|

| Click here to view our Master Premium Account Agreement |

- Alternate Currency: Means the currency in which we buy the Base Currency from you, in the event we choose to exercise the Currency Option

- Base currency: Means the currency in which you agree to sell us the Currency Option and the currency in which the Initial Investment is made.

- Currency Option: Means the right (but not the obligation) for Citibank NA, to convert your Initial Investment and Option Premium into the Alternate Currency at the Strike Rate at maturity.

- Expiry Date: Means the date on which your Premium Account expires and the date on which we determine if the payment is made to you of the Initial Investment and Option Premium in either the Base or Alternative currency.

- Maturity Date: Means the date on which your Premium Account matures and the date on which we pay you the Initial Investment and Option Premium.

- Initial Investment: Means the initial principal sum invested by you and which we may buy back from you in the Alternate Currency (The minimum investment amount is US$25,000 or equivalent)

- Option: An Option is a financial instrument that specifies a contract between two parties for a future transaction on an asset at a reference price. The buyer of the Option gains the right, but not the obligation, to engage in that transaction, while the seller incurs the corresponding obligation to fulfill the transaction. The underlying asset can be a stock, a bond, a currency or a future. In a Premium Account, Citibank NA. will buy a Currency Option from you.

- Option Premium: Means the premium payable by us to you as consideration for you granting us the Currency Option.

- Strike Rate: Means the pre-agreed exchange rate of one unit of the Base Currency into the Alternate Currency

- Tenor: Means the period of time from when the Premium Account begins until the Maturity Date. The Tenor will normally range from one-week to three-months.

|

Click on  to expand and on to expand and on  to minimise the details. to minimise the details. |

|

| What is Citibank Premium Account and how does it work? |

|

| Citibank Premium Account is in substance an investment in one or more foreign currencies. It is subject to foreign exchange rate fluctuations, which may provide opportunities and risks. |

|

| To apply for a Premium Account, please visit your nearest branch where our relationship manager will assist you in the account opening process including assessment of your investor profile and your knowledge and experience. |

|

|

4 Steps to Establish a Citibank Premium Account:

|

|

|

|

|

Here's an example:

|

|

| Assuming that you have invested an amount of 100,000 USD in a one-week Citibank Premium Account, with US Dollar as your base currency and British Pound (GBP) as your alternate currency. |

|

Strike Rate (Pre-agreed Exchange Rate): GBP/USD 1.5500

Interest rate: 7.57% p.a.*

Current Exchange Rate: GBP/USD 1.5550 |

|

| At maturity, you will be paid on the weaker of the two currencies.

There are two possible scenarios: |

|

|

|

|

Scenario 1 |

|

Scenario 2 |

|

|

Rate on Expiry Date1 |

|

USD Weakens to 1.5650 |

|

USD Strengthens to 1.5400 |

|

Payout Currency^ |

|

Principal and interest

will be paid in USD |

|

Principal and interest

will be paid in GBP |

|

|

Principal + Interest received |

|

USD 100,147 |

|

GBP 64,610

(USD 100,147/1.5500) |

|

|

|

| * This is an indicative rate for a USD Premium Account of USD 100,000 with GBP as the alternate currency, strike price 50 points away from the prevailing spot rate as of April 29, 2013 for a one-week tenor. |

|

** The above is for demonstration purposes only and shall not be construed as investment advice. Citibank does not offer investment or tax advice to its customers. |

|

| 1Expiry Date is 2 business days before maturity date.

^ In the event that the market rate on Expiry Date is equal to the strike price, the Bank reserves the right to pay your principal plus interest in either the base currency (USD 100,147) or the alternate currency (GBP 64,610). |

|

|

|

| What is the minimum amount required to establish a Citibank Premium Account Online? Any pre-requisites involved? |

|

| The minimum amount for establishing a Citibank Premium Account is USD 25,000 (or equivalent). |

|

| However, you would also need to have signed a Citibank Premium Account Master Agreement, Risk Disclosure and completed the Investment Risk Profile before proceeding to establish a Citibank Premium Account. |

|

| To apply for a Premium Account, please visit your nearest branch where our relationship manager will assist you in the account opening process including assessment of your investor profile and your knowledge and experience. |

|

| If you would like a Citibank relationship manager to call you, please click here |

|

|

|

|

|

|

|

|

|

| What does it mean when my Citibank Premium Account deal is "Lapsed" or "Exercised"? |

|

| When a Citibank Premium Account expires, the system will determine whether the Citibank Premium Account deal is lapsed or exercised by comparing the pre-agreed Strike Rate of the currency pair against the prevailing exchange rate of the currency pair. |

|

| E.g. USD Base against AUD Alternate at the Strike Rate of AUD/USD 1.251 |

|

| If the base currency weakens against the alternate currency (from AUD/USD 1.266 to 1.270), the deal is determined as "Lapsed". You will then receive the principal and interest earned in the base currency (USD). |

|

| If the base currency strengthens against the alternate currency (from AUD/USD 1.266 to 1.243), the deal is determined as "Exercised". You will then receive the principal and interest earned converted to the alternate currency (AUD) at the pre-agreed exchange rate of 1.251 (i.e., Principal + Interest computed in USD and converted to AUD). |

|

|

|

| I have just signed the Citibank Master Premium Account Agreement at the branch. Can I book my Premium Accounts online now? |

|

| Your Citibank Master Premium Account Agreement and Investment Risk Profile forms are forwarded to our Treasury Unit for processing and review before it is availed for online usage. In general, it takes 24 hours for processing. |

|

| However even after processing, your first Premium Account transaction has to be booked through our Treasury Service Office over a recorded phone line. Thereafter, from the second deal onwards you can log on to: online.citibank.ae to book Premium Accounts online. |

|

|

|

|

| Can I convert my base currency when I renew a Citibank Premium Account deal online? |

|

| If your deal has lapsed, you have the option to change the base currency when you book a new Citibank Premium Account deal. On the other hand, if your Citibank Premium Account is exercised, i.e. your fund is converted to the alternate currency; you can only use the currency which the previous Citibank Premium Account deal had exercised into, as the base currency of the new Citibank Premium Account. |

|

|

|

|

|

|

| Disclaimer : |

|

The commission charged on Premium Accounts is a maximum of 8 % per annum of the principle amount invested. Further details can be provided on request. |

|

This is a Non-Advised product. Citibank UAE does not offer any recommendation for specific transaction with Currency Pairs, Tenors and Strike Levels (all 3 combined). |

|

A Citibank Premium Account is a dual currency investment that involves a currency option which confers on the bank the right to repay the principal and interest earned at maturity in either the base currency or alternate currency. Part or all of the interest earned at maturity on the Citibank Premium Account represents the premium that the bank pays for the currency option. |

|

By investing in a Citibank Premium Account, you are giving the bank the right to repay you at a future date in the alternate currency (instead of the base currency in which your initial investment was made), regardless of whether you wish to be repaid in the alternate currency at that time.

Unlike a traditional bank account, a Citibank Premium Account has an investment element and returns may vary. Citibank Premium Accounts are subject to a number of risks, including foreign exchange fluctuations, which may provide both opportunities and risks. You may experience a foreign exchange loss when you convert any alternate currency into the base currency, which may neutralize the interest earned at maturity and may even result in losses to the principal. It may happen if the alternate currency depreciates in value against the base currency and the interest earned at maturity will not compensate for the foreign exchange loss, which in that case will be incurred when the principal and premium received in the alternate currency are converted back into the base currency. Exchange

controls may also apply to currencies your Citibank Premium Account is linked to. For more information on a Citibank Premium Account, you should carefully read the terms and conditions of the Citibank Premium Account.

You should note that a Citibank Premium Account is an investment product that should be held to maturity. Early withdrawal of a part of a Citibank Premium Account prior to the maturity date is not permitted. Early withdrawal of the whole of a Citibank Premium Account is permitted but strongly discouraged, because you will have to pay early termination charges as determined by the bank, and these charges will be deducted from the amount repaid under the Citibank Premium Account. You should also note that the bank may, at any time at its discretion, discharge its entire liability with respect to a Citibank Premium Account by paying

you your principal and interest that has accrued in the base currency or a currency of the Bank's choice. |

|

| This website does not constitute any offer or solicitation to buy or sell. Investors should refer to the relevant offering document(s) for detailed information and applicable terms & conditions prior to subscription. Investment products are not bank deposits or obligations or guaranteed by Citibank N.A., Citigroup Inc. or any of its affiliates or subsidiaries unless specifically stated. Investment products are not insured by government or governmental agencies. Investment and Treasury products are subject to Investment risk, including possible loss of principal amount invested. Past performance is not indicative of future results: prices can go up or down. Investors investing in investments and/or treasury products denominated in foreign (non-local) currency should be aware of the risk of exchange rate fluctuations that may cause loss of principal when foreign currency is converted to the investors home currency. Investment and Treasury products are not available to U.S. persons. All applications for investments and treasury products are subject to Terms and Conditions of the individual investment and Treasury products. Customer understands that it is his/her responsibility to seek legal and/or tax advice regarding the legal and tax consequences of his/her investment transactions. If customer changes residence, citizenship, nationality, or place of work, it is his/her responsibility to understand how his/her investment transactions are affected by such change and comply with all applicable laws and regulations as and when such becomes applicable. Customer understands that Citibank does not provide legal and/or tax advice and are not responsible for advising him/her on the laws pertaining to his/her transaction. Citibank UAE does not provide continuous monitoring of existing customer holdings. |

|

|

|

|